Why Policy2 Now Matters More Than Supply

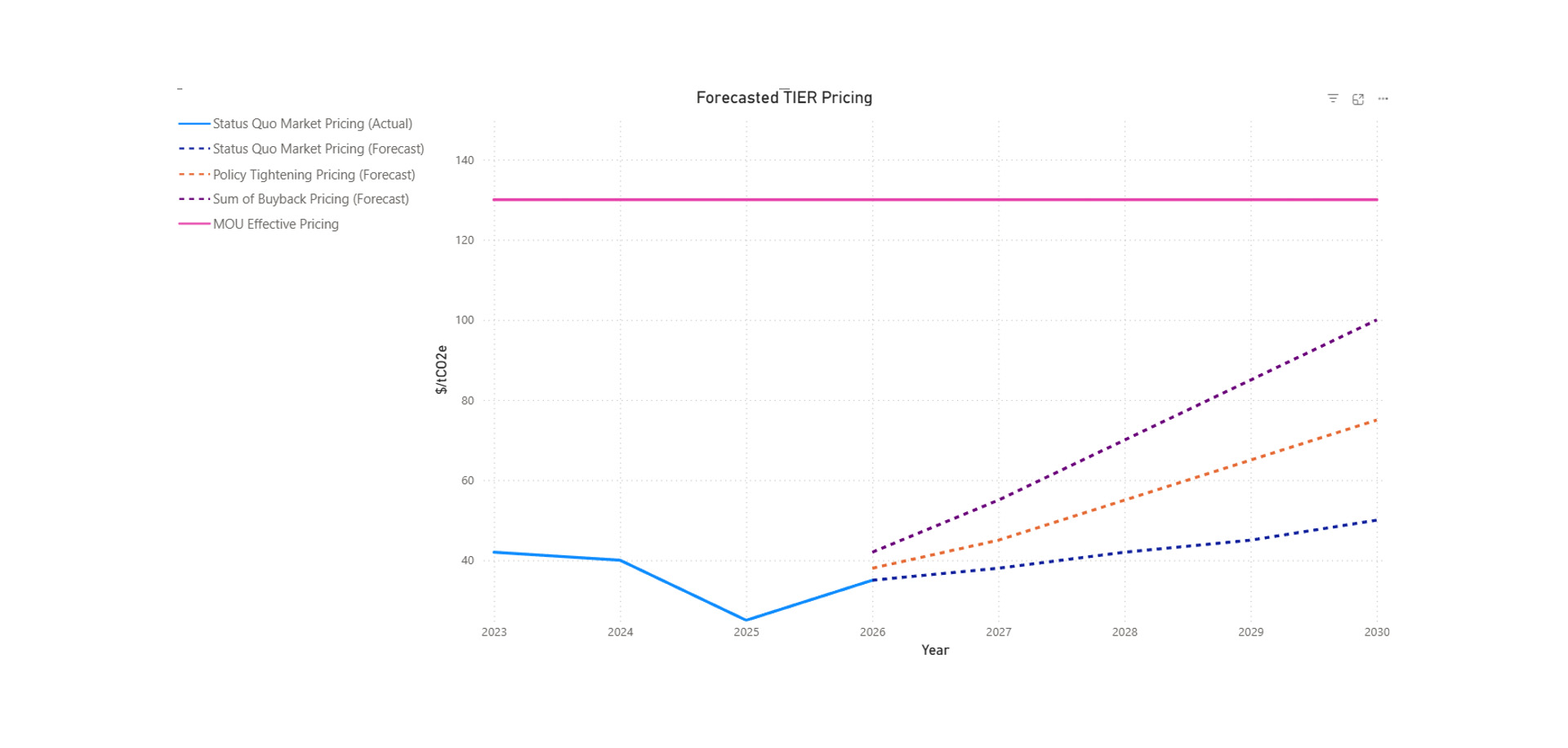

With Alberta’s carbon market appearing to be tightening on fundamentals alone, policy choices now determine the speed, shape, and magnitude of price outcomes. The federal Alberta Memorandum of Understanding (MOU) introduces a critical reference point: a $130 effective carbon price, a level that closely aligns with estimated breakeven economics for large-scale projects such as Pathways Alliance CCUS.

Reaching that level is not optional if Alberta intends to support large-scale decarbonization. The remaining question is how the market gets there.

The Federal–Alberta MOU and the $130 Signal

The $130 figure should be understood as a policy benchmark, not an immediate price target. Its timing matters:

- A gradual path allows tightening fundamentals to close much of the gap organically.

- A compressed timeline implies additional policy intervention will be required.

The MOU, therefore, acts as a signal shaping expectations rather than a single forecasted outcome.

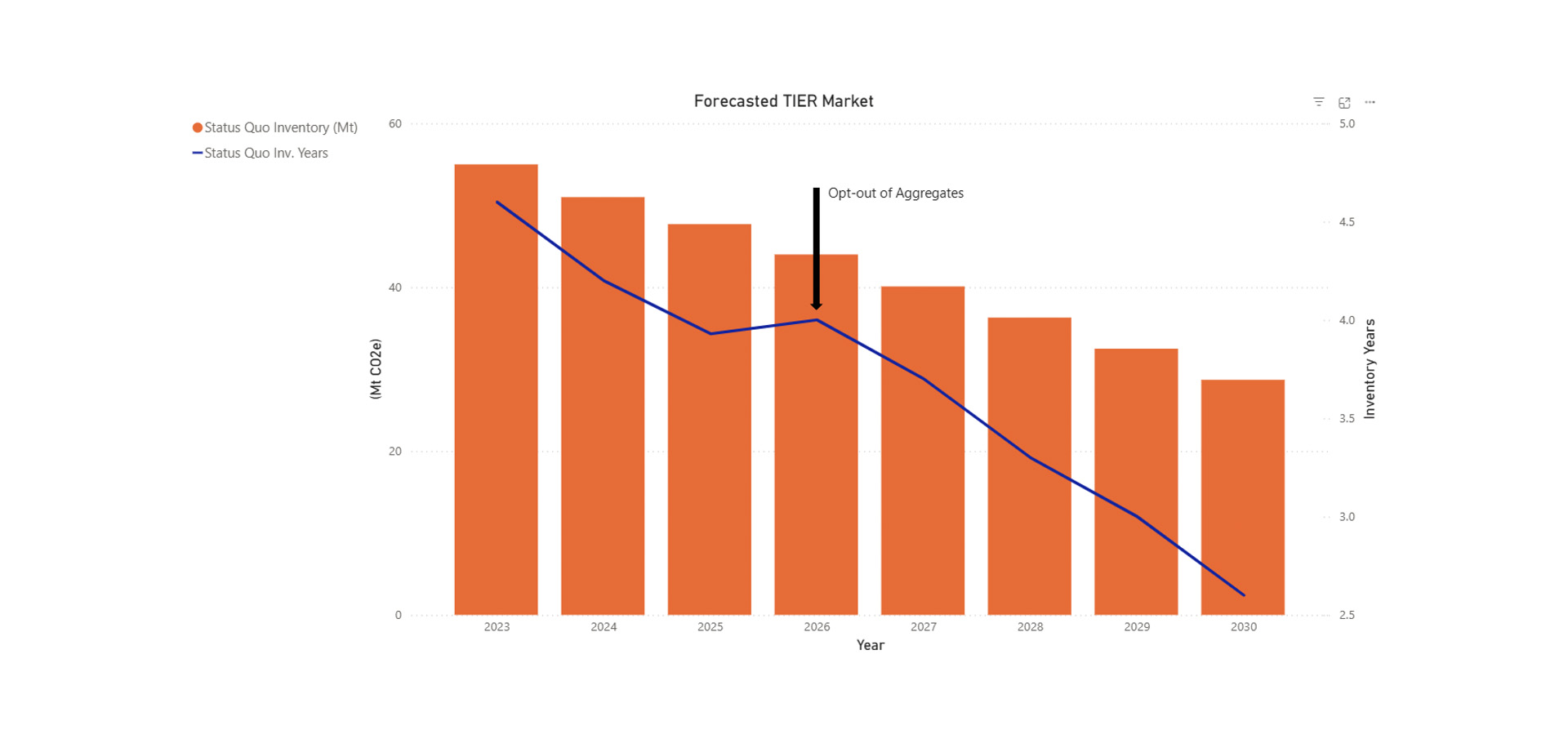

Status Quo Market Conditions

Using current market conditions and trajectories, if left alone, the market appears to be heading towards lower inventory, but would take multiple years to get there.

Policy Levers Alberta Could Pull

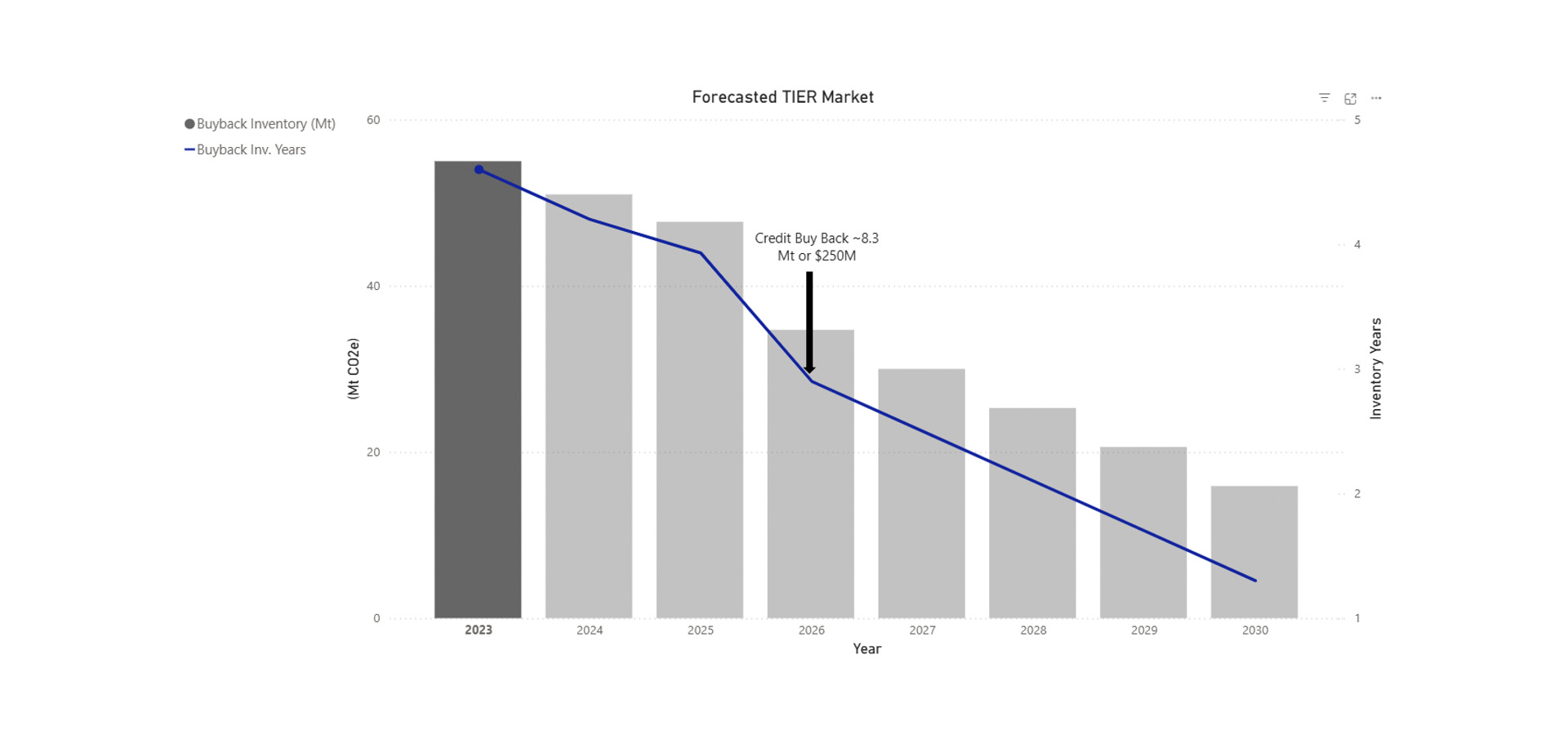

Offset Buybacks (The “Share Buyback” Analogy)

The Alberta TIER fund is estimated to hold approximately $1.1 billion. With roughly $466 million collected from 2024 compliance alone and typical annual expenditures of around $130 million, there appears to be financial capacity for credit buybacks.

Using TIER funds to purchase and retire offsets would immediately reduce inventory, strengthen price signals, and accelerate investment into emissions reduction.

Modelled scenarios show that a roughly $250 million buyback beginning in 2026, removing approximately eight million tonnes from active supply, would rapidly compress inventory years and accelerate the transition from a buyer’s market to a seller’s market.

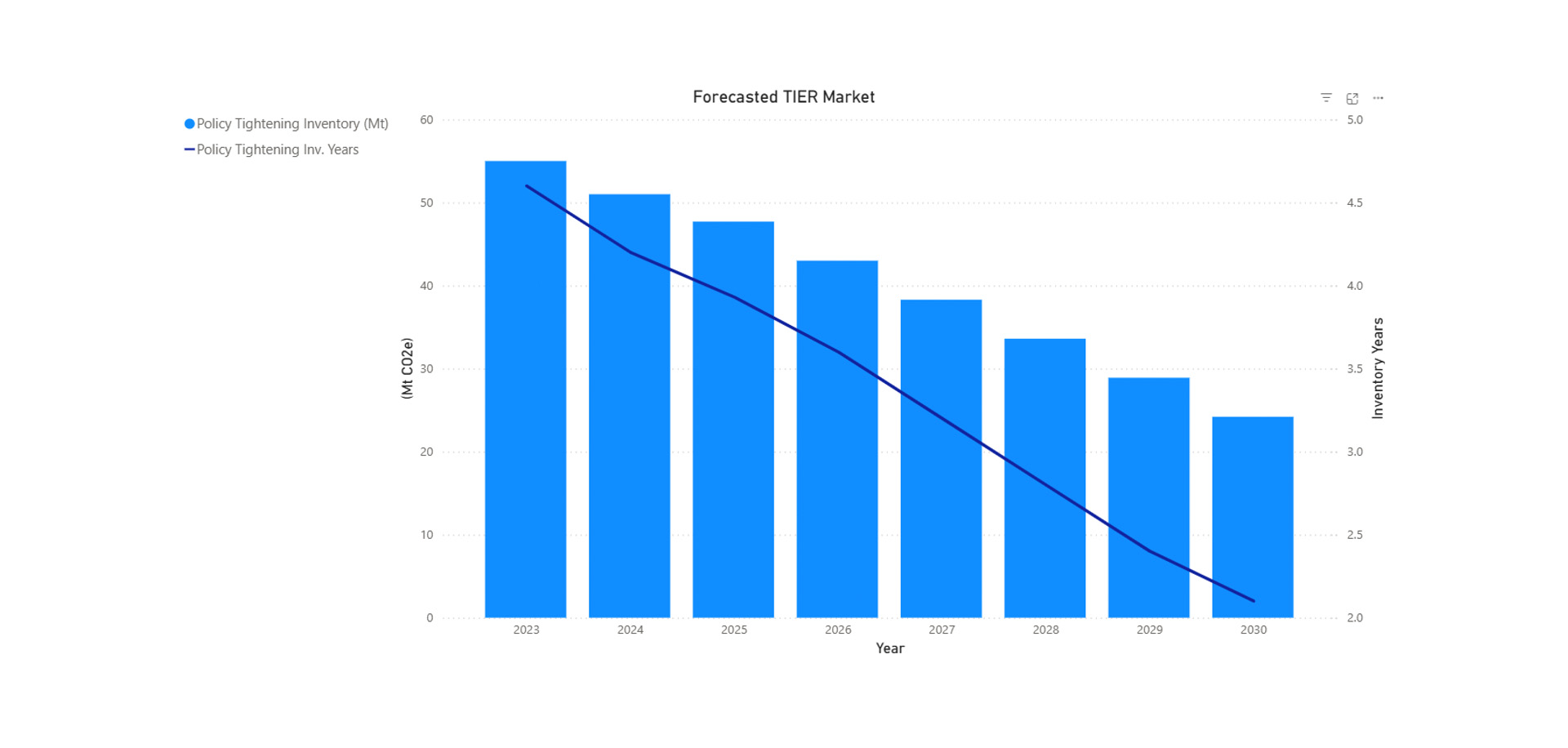

Increasing Benchmark Stringency

Incremental increases in benchmark stringency would raise compliance demand and accelerate credit retirements.

Modeling a one percentage point increase applied system-wide, with most TIER facilities moving from a 2 percent to a 3 percent requirement and oil sands facilities moving from 3 percent to 4 percent, shows that even modest adjustments can materially tighten the system.

The primary challenge with this lever is the added cost burden on regulated industries that already face global competitiveness pressures.

Cross-Provincial Fungibility

Allowing offsets to move across Canada’s fragmented markets could:

- Smooth regional imbalances

- Improve price discovery

- Increase decarbonization efficiency

Implementation is complex due to regulatory fragmentation, jurisdictional authority concerns, and competitiveness issues but the lever remains powerful.

Other Market Considerations

Upstream Oil & Gas Aggregates (Market Condition)

Historically, upstream oil and gas aggregates have represented approximately 8 to 12 percent of annual offset retirements, equivalent to roughly 1.0 to 1.5 million tonnes per year of compliance demand. With aggregates now able to opt out, annual retirements could decline by a similar percentage, slowing near-term inventory drawdown and reducing price pressure relative to a status quo scenario. Even under this outcome, however, aggregate removal would not reverse the broader tightening trend, as inventory years remain below four and other demand drivers persist.

Data Centre’s as Structural Demand

Canada and Alberta are actively positioning themselves as destinations for large data centre development. At scale, data centres represent long-lived, electricity-intensive facilities that can materially increase compliance obligations under TIER.

While this demand has not yet appeared meaningfully in registry data, it represents a structural source of future compliance demand that is additive to existing industrial emitters.

Pathways & Direct Investment

Pathways Alliance CCUS, if implemented at scale, could reduce compliance demand by capturing emissions that would otherwise require offsets or performance credits. Federal estimates suggest up to approximately 4.2 million tonnes of CO₂ per year could be captured by 2030, with longer-term expansion potential reaching up to 20 million tonnes annually.

Alberta’s evolving TIER framework also allows facilities to meet compliance through direct investment in emissions-reducing technologies rather than through offset retirement alone. While this option can reduce near-term offset demand, it appears relatively unattractive compared to purchasing credits due to higher upfront capital requirements, execution risk, and long payback periods.

As long as offsets or EPCs remain available at competitive levels, direct investment is likely to remain a secondary compliance pathway.

Sustained higher prices could also unlock new, more capital-intensive offset supply that is uneconomic at lower price levels. Any such increase in issuance would occur in response to tightening conditions rather than ahead of them.

Scenario Modeling and Price Implications

Bringing these forces together, scenario modelling helps illustrate how different combinations of policy action and market response could shape outcomes. Under a status quo trajectory, Alberta’s carbon offset inventory continues to decline steadily through the end of the decade, with inventory coverage compressing from just under four years today to roughly 2.5 years by 2030. This outcome alone suggests a structural imbalance already present in the market.

Under modest policy-tightening assumptions, such as incremental increases in benchmark stringency, inventory drawdown accelerates and compliance flexibility diminishes. In a buyback scenario, a single discrete intervention materially alters market psychology by compressing the timeline over which the market is asked to respond.

Pricing outcomes reflect these dynamics. Inventory tightening alone does not determine prices; expectations, confidence, and policy signals play an equally important role. The modeled price trajectories are therefore bounded scenarios rather than a single forecast. The $130 value referenced in the federal–Alberta MOU should be interpreted as a policy benchmark that signals the economics required to support large-scale decarbonization, not as a near-term guaranteed market price.

Final Takeaway

Stepping back from individual levers and scenarios, the overarching direction of the market becomes clear. Regardless of the specific policy path chosen, Alberta’s carbon market is tightening. Without policy intervention, inventory continues to decline. With policy action, that decline accelerates.

Either way, higher prices were always implied by the underlying math. The market was not broken; it was constrained by uncertainty. As clarity returns, both fundamentals and policy are now aligned toward a structurally tighter and more investable carbon market.

Colin Gendre

Director of Carbon Strategies

Colin Gendre is Director of Carbon Strategies at Intricate, where he leads the development and execution of carbon offset project development. With more than 20 years of experience spanning instrumentation, controls, automation, and emission services, he helps clients translate complex carbon projects into practical, scalable systems. Since joining Intricate in 2012, Colin has played a central role in building emission-focused services that align technical rigor with evolving regulatory and market demands.